The maritime industry is currently navigating one of its most transformative and critical phases in history, driven by an urgent, worldwide consensus to significantly reduce greenhouse gas emissions originating from the shipping sector. As global stakeholders, policymakers, and manufacturers collaborate more closely than ever before, the shift toward sustainable practices is reshaping traditional operational models and laying the foundation for a carbon-neutral maritime ecosystem. This comprehensive maritime decarbonization market forecast 2025-35 provides an in-depth analysis of these systemic shifts, focusing on the technological advancements, regulatory pressures, and shifting consumer demands that are fundamentally redefining global shipping. By exploring the multifaceted layers of this transition, from the rapid emergence of alternative fuel sources to the rigorous implementation of international environmental standards, Transport Advancement outlines the critical trajectory of the sector. The integration of sustainable solutions is no longer a distant ambition but an immediate necessity for industry stakeholders seeking to maintain operational viability and competitive advantages in a rapidly evolving, eco-conscious global economy.

Market Size and Forecast Data

The financial scope of this environmental transition is vast and rapidly accelerating. According to the data evaluated in this report, the maritime decarbonization market was valued at 16.15 USD Billion in the base year of 2024. This valuation serves as a foundational baseline for a period of robust, uninterrupted expansion over the next decade. By the end of 2025, the market size is projected to experience notable growth, reaching an estimated 17.7 USD Billion. However, the most significant expansion is forecast to occur over the subsequent ten years. By the year 2035, the market valuation is expected to surge to an impressive 44.31 USD Billion.

Throughout this forecast period from 2025 to 2035, the industry is anticipated to exhibit a strong Compound Annual Growth Rate (CAGR) of 9.61%. This substantial financial trajectory underscores the massive scale of capital deployment, research, and infrastructure development required to meet ambitious global climate targets. Investments in research and development are surging, as there is a collective recognition across the sector of the absolute necessity for advanced, emission-reducing technologies that can concurrently enhance long-term energy efficiency.

Key Market Drivers Accelerating the Transition

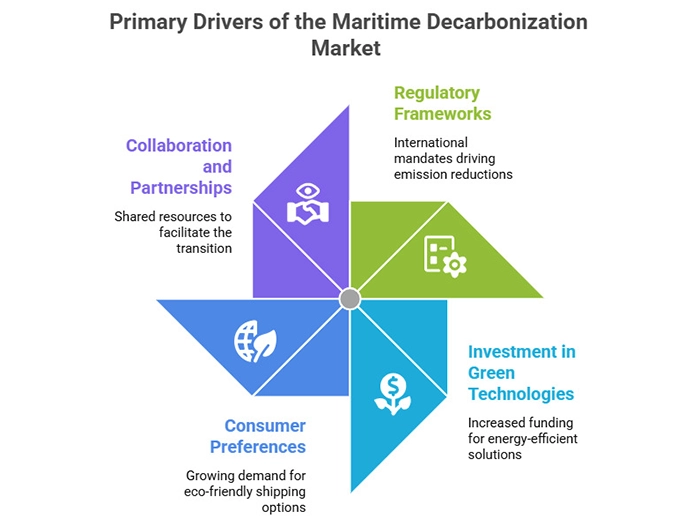

The robust growth trajectory detailed within the industry is propelled by several interwoven market drivers, chief among them being the establishment of stringent international regulatory frameworks. Regulatory bodies, most notably the International Maritime Organization (IMO), have instituted ambitious mandates designed to reduce total annual greenhouse gas emissions from international shipping by at least 50% by 2050. This rigorous regulatory environment acts as a structural catalyst, compelling shipping entities to aggressively pivot toward cleaner technologies. While the capital investment required to achieve compliance can act as a barrier for some operators, organizations that proactively adapt are heavily favored to secure distinct competitive advantages, thereby stimulating further market expansion.

Furthermore, direct investment into sustainable shipping technologies is witnessing a remarkable surge. The urgent need to comply with international regulations has resulted in a recorded 30% increase in investments targeting green technologies, such as energy-efficient hull designs and wind-assisted propulsion systems, over the past year. These investments not only address environmental sustainability metrics but also deliver tangible improvements in overall operational efficiency, drawing an increasing number of stakeholders into the market.

Another powerful driver reshaping the landscape is the distinct shift in consumer preferences toward eco-friendly shipping alternatives. Consumer awareness regarding climate change has reached unprecedented levels, and there is a growing economic preference for corporations that demonstrate a verifiable commitment to sustainable practices. Data indicates that nearly 60% of consumers are now willing to pay a premium for goods that have been transported via environmentally responsible and carbon-neutral methods. This undeniable consumer demand forces shipping providers to expedite the integration of decarbonization strategies to remain economically viable. To navigate these pressures, the sector is also experiencing a rise in collaboration and partnerships among various stakeholders, allowing for shared resources and reduced operational costs during this complex transition.

Strategic Shifts and Technological Innovations

A central theme within any thorough analysis of the market is the rapid pace of technological innovation, which is fundamentally enhancing the emission reduction capabilities of the entire shipping sector. The industry is actively pursuing a departure from conventional fossil fuels by investing heavily in alternative fuel ecosystems. Concurrently, hardware and software innovations are being aggressively developed to minimize fuel consumption. Advancements such as highly advanced hull designs and wind-assisted propulsion systems are at the forefront of this mechanical revolution.

Moreover, the market is recognizing the critical role of specialized emission reduction systems. Innovations like sophisticated carbon capture and storage (CCS) systems and advanced hydrogen fuel cells have emerged as highly viable, long-term solutions. Reflecting their growing importance, the sub-market for these specific emission reduction technologies is projected to expand dramatically, with estimates indicating a compound annual growth rate exceeding 20% over the coming years. Furthermore, the integration of cutting-edge digital solutions, including artificial intelligence (AI) and deep data analytics, is anticipated to play an increasingly pivotal role in optimizing vessel routes, managing fuel consumption dynamically, and maximizing overall operational efficiencies.

Market Segmentation: Shifting Fuel Types

The maritime decarbonization market has several choices of fuels, with the primary focus on these fuel types: Green Ammonia, Hydrogen, and Bio-methanol.

Currently, Green Ammonia stands as the dominant fuel type, capturing the largest segment of the market share. The ascendancy of Green Ammonia is attributed to its highly favorable characteristics, including a superior energy density and its unique ability to be integrated into much of the existing ammonia infrastructure. Because it can be produced utilizing renewable energy sources, it represents a highly effective alternative to traditional fossil fuels for operators prioritizing immediate, scalable carbon reduction.

Conversely, Hydrogen is officially recognized as the fastest-growing alternative fuel within the segment. Hydrogen offers immense potential due to its remarkable ability to produce absolutely zero greenhouse gas emissions at the point of combustion. Consequently, it has attracted significant long-term interest, particularly for supporting zero-emission mandates in long-distance maritime transport. However, the widespread adoption of Hydrogen is currently tempered by the necessity for massive infrastructure development and further technological breakthroughs in safe storage and handling.

Bio-methanol, while presently holding a smaller overall market share compared to Green Ammonia and Hydrogen, is steadily gaining strategic traction. Its primary advantage lies in its seamless compatibility with existing marine engines and current bunkering infrastructure, making it a highly attractive transition fuel.

Market Segmentation: Application Dynamics

In terms of application, the market is broadly divided into Ships, Ports, and Others. The ships segment currently dominates the market, holding the largest overall market share. This dominance is a direct reflection of the massive capital being deployed to retrofit thousands of existing vessels, ranging from massive container ships to bulk carriers, while simultaneously integrating green technologies into entirely new shipbuilding projects. By 2025, the market valuation dedicated exclusively to the ships segment is projected to hit 22.0 USD Billion.

However, the ports segment is emerging as the fastest-growing application within the sector. Ports are undergoing rapid, systemic evolution as they integrate cleaner energy sources and develop smart, sustainable infrastructure initiatives. This rapid growth is necessitated by the requirement for ports to successfully accommodate and service the new generation of greener vessels, while also reducing their own localized carbon footprints.

Regional Distribution of the Maritime Decarbonization Market

The geographic distribution of the market reveals distinct regional shifts and varied rates of technological adoption across the globe.

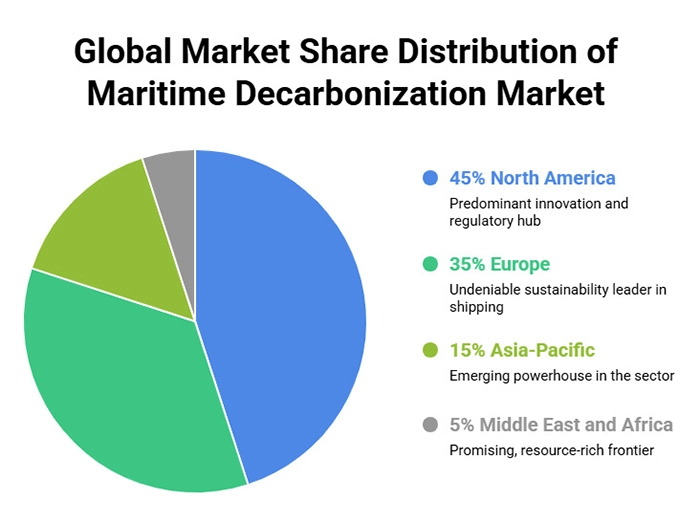

North America currently operates as the predominant innovation and regulatory hub, commanding the largest global market share at approximately 45%. The robust market presence in the United States and Canada is largely fueled by stringent governmental regulations, including aggressive initiatives championed by the Environmental Protection Agency (EPA). Furthermore, lucrative government incentives for green technologies and deep investments in local research and development ensure North America remains at the vanguard of the industry.

Europe follows closely, positioned as the undeniable sustainability leader in shipping with a market share of roughly 35%. The European market is powerfully catalyzed by sweeping legislative frameworks like the European Union’s Green Deal, combined with a staunch regional commitment to achieving net-zero emissions by the year 2050. The strategic advantage of having major, forward-thinking shipping hubs, such as the ports located in the Netherlands and Germany, further solidifies Europe’s strong market position.

Meanwhile, the Asia-Pacific region is recognized as the emerging powerhouse in the sector, currently holding about 15% of the global market share. Driven by immense economic growth, rapidly expanding global trade routes, and tightening regulatory pressures in major manufacturing nations like China and Japan, the Asia-Pacific region is investing heavily in sustainable solutions to modernize its massive shipping lanes.

Finally, the Middle East and Africa region, currently accounting for about 5% of the global market, represents a highly promising, resource-rich frontier. Leveraging its strategic geographic proximity to major international trade routes and its vast natural resources, this region is slowly beginning to implement environmental regulations and actively seeks to diversify its economic portfolio through investments in emerging green technologies.

Future Outlook

Looking forward, the maritime decarbonization market is set for a profoundly robust future. By 2035, the sector is expected to be fundamentally transformed by strict regulatory compliance and the mainstream maturation of innovative solutions. Significant, untapped opportunities continue to lie in the advanced development of specialized hydrogen fuel cell technologies designed specifically for marine environments, as well as the widespread, scalable implementation of carbon capture and storage solutions. Furthermore, the expansion of renewable energy sources for port operations presents a vital avenue for continuous growth. Transport Advancement notes that the maritime industry’s unwavering commitment to decarbonization will not only reshape the future of global logistics but also play a pivotal role in the worldwide fight against climate change, solidifying a sustainable, clean-energy legacy for decades to come.

{kind=link}