The port material handling equipment vehicle market encompasses specialized mobile machinery used within the secured perimeters of maritime ports, inland container depots, and intermodal rail terminals to transport, stack, and position diverse cargo types including containers, bulk goods, and roll-on/roll-off (Ro-Ro) loads.

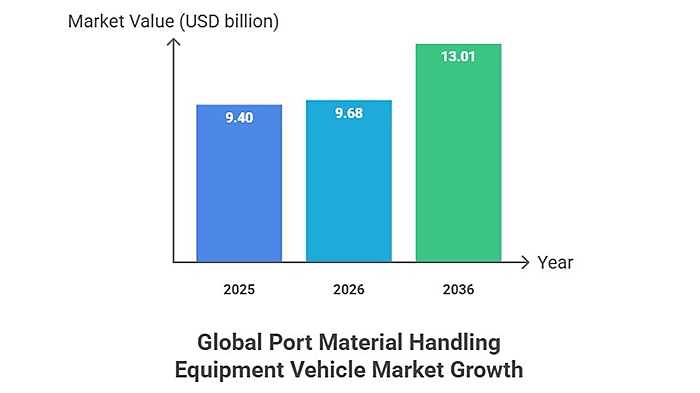

The global maritime logistics sector is currently undergoing a significant transformation, driven by a convergence of regulatory pressures, technological advancements, and shifting trade patterns. According to forecast of the Port Material Handling Equipment Vehicle Market Report 2026, the market for specialized port vehicles is valued at USD 9.68 billion in 2026. Following a valuation of USD 9.40 billion in 2025, the industry is projected to expand at a compound annual growth rate (CAGR) of 3.0% between 2026 and 2036, eventually reaching a market size of USD 13.01 billion. This steady growth trajectory is underpinned by dual investment cycles: terminal operators must simultaneously expand handling capacity to manage congested facilities while transitioning their aging diesel-powered fleets toward sustainable hybrid and electric alternatives.

Primary Market Drivers and Forecast Shifts

Several critical factors are reshaping the procurement landscape for port machinery. A primary driver is the International Maritime Organization (IMO) 2023 greenhouse gas strategy, which targets net-zero emissions from international shipping by 2050. These decarbonization expectations now extend directly to port-side operations, forcing terminal operators in major hub ports across North America and Europe to include electrification readiness as a standard procurement specification for all new vehicle orders.

Beyond environmental mandates, the port material handling equipment vehicle market identifies the continuous expansion of global trade volumes and the modernization of port infrastructure as essential growth catalysts. Governments worldwide are increasingly allocating funds to improve port and waterway efficiency for instance, the USA has dedicated over USD 17 billion to such improvements under the Infrastructure Investment and Jobs Act. Furthermore, the decline in technology costs for electric components and autonomous systems is enabling broader market penetration, allowing smaller terminal operators to adopt high-efficiency handling solutions that were previously reserved for premium, high-volume segments.

Detailed Segment Analysis of the Market by Vehicle Type

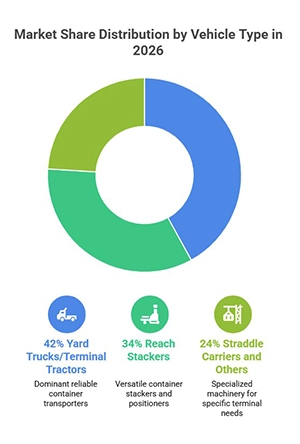

The market is categorized into several distinct vehicle types, each serving specialized roles within the terminal environment. In 2026, the distribution of market share by vehicle type is as follows:

- Yard Trucks/Terminal Tractors: This segment holds a dominant 42.0% market share in 2026. These vehicles are essential for transporting containers within terminals due to their proven reliability and established operational integration. While they maintain leadership, they face increasing pressure to transition toward electric power and may eventually compete with automated guided vehicles in highly modernized ports.

- Reach Stackers: Accounting for 34% of the market, reach stackers are favored for their versatility in container stacking and flexible positioning. Their growth is driven by the need for space optimization in expanding container terminals where operational efficiency is paramount.

- Straddle Carriers and Others: This segment represents 24% of the market. It includes specialized machinery such as straddle carriers, heavy-duty forklifts, and rubber-tyred gantry carriers tailored for specific terminal configurations. While growth here is more moderate, these vehicles remain vital for bulk cargo and niche terminal operations.

Detailed Segment Analysis of the Market by Power Type

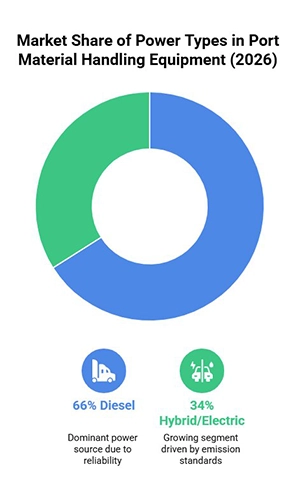

One of the most significant shifts highlighted in the port material handling equipment vehicle market is the evolution of power sources. As of 2026, Diesel remains the largest power segment with a 66.0% market share. This dominance is attributed to a mature technology base, standardized maintenance procedures, and structural demand from heavy-duty applications where diesel’s reliability is well-established.

However, the Hybrid/Electric segment, currently holding a 34% share, is poised for explosive growth through 2030. This shift is fueled by stringent emission benchmarks and zero-emission mandates that provide long-term operational cost advantages and regulatory compliance. While higher initial capital costs and the need for charging infrastructure remain restraints, advancements in battery technology are gradually overcoming these barriers in heavy-duty port applications.

Detailed Segment Analysis of the Market by End User Type

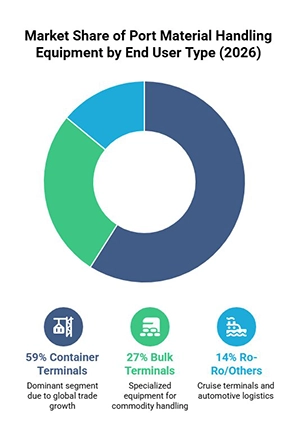

The primary end-user of port material handling equipment is the Container Terminal segment, which commands 59.0% of the market share in 2026. This dominance is a direct result of the global growth in containerized trade and the ongoing push for terminal automation to optimize throughput. Bulk Terminals follow with a 27% share, requiring specialized equipment for managing commodities like coal, grain, ore, and liquid bulk. The Ro-Ro/Others segment, including cruise terminals and automotive logistics facilities, accounts for 14% share in 2026.

Regional Market Analysis and Projections

The market exhibits diverse growth dynamics across different geographic regions, influenced by local trade policies, infrastructure funding, and environmental regulations.

America: U.S. Becomes The Growth Leader

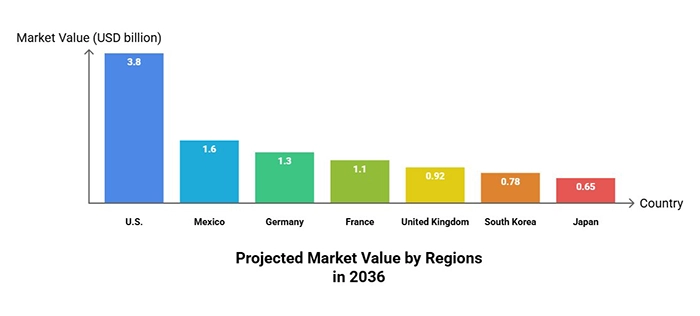

The U.S. is projected to lead global market growth with a 3.5% CAGR through 2036. Driven by federal infrastructure excellence programs, revenue in the USA is expected to reach USD 3.8 billion by 2036. Major port authorities in regions like Los Angeles, Long Beach, and New York/New Jersey are establishing comprehensive procurement programs to modernize logistics and meet growing demand for efficient cargo handling.

Mexico follows a strong trajectory with a 3.2% CAGR, reaching a projected value of USD 1.6 billion by 2036. Growth in Mexico is primarily supported by the “nearshoring” trend, which has led to increased container volumes at Pacific and Gulf coast ports such as Lazaro Cardenas and Manzanillo.

Europe: Innovation and Modernization

The European market is projected to grow from USD 2.5 billion in 2026 to USD 3.3 billion by 2036, at a 2.8% CAGR.

- Germany maintains regional leadership with a 29.2% share in 2026, reaching a value of USD 1.3 billion by 2036. The focus here is on terminal modernization programs in Hamburg and Bremerhaven, prioritizing high-quality, sustainable equipment.

- France tracks a growth path toward USD 1.1 billion by 2036, a market share of 2.8%, with investments in Marseille and Le Havre focusing on automated handling systems.

- The United Kingdom, despite post-Brexit adjustments, is expanding its port modernization efforts to reach a value of USD 920 million and a market share of 2.6% by 2036, particularly through capacity expansions at Felixstowe and London Gateway.

Asia Pacific: Precision and Smart Integration

- South Korea is advancing at a 2.5% CAGR, aiming for a USD 780 million market by 2036. The market focus here is on “smart port” applications, integrating advanced automation with traditional maritime excellence.

- Japan follows a 2.4% CAGR toward a value of USD 650 million. Japanese market dynamics are defined by exceptionally high quality standards and unique requirements for earthquake-resistant port equipment, including seismic safety systems and disaster preparedness integration.

Competitive Landscape and Strategic Implications

The competitive environment is shifting from basic equipment manufacturing toward fully integrated, specification-tight solutions. Value is increasingly migrating to equipment that offers automation compatibility, environmental compliance, and documented performance premiums. Terminal operators now prioritize “compliance-first” procurement, where equipment must meet regulatory certifications before even being considered for tender shortlists.

Furthermore, technology partnership investments are becoming critical. By forming alliances with technology providers, equipment manufacturers can deliver end-to-end solutions, such as remote monitoring and predictive maintenance, which standalone suppliers cannot match in competitive bids. High switching costs, including terminal layout modifications and staff retraining, often stabilize the position of incumbent providers, but the disruption caused by electrification and automation mandates is creating new opportunities for innovative designs.

Conclusion

The port material handling equipment vehicle market is positioned for sustained expansion through 2036. As international trade continues to grow and environmental regulations tighten, the demand for high-efficiency, low-emission, and automated handling vehicles will only intensify. Market participants who prioritize certified compliance with evolving standards and demonstrate seamless integration with existing smart port infrastructure will be best positioned to capture contract volumes in this multi-year procurement cycle. Organizations that delay capital commitments toward fleet modernization risk operational obsolescence as global standards for terminal productivity and environmental responsibility become increasingly stringent.

{kind=link}